Executive Briefing

Why Square’s Cash App is on fire

Stimulated by the stimulus, Square is building a modern bank with some personality.

By Dan Frommer on Wednesday, August 12, 2020 at 8:00 am

By Dan Frommer on Wednesday, August 12, 2020 at 8:00 am

The coronavirus pandemic has been brutal for small retail businesses: Square, which handles payment processing for many of them, reported that its gross processing volume declined 15% year over year in the second quarter, compared to more than 25% growth in 2019.

But Square’s other business, the consumer payments and banking service called Cash App, is booming, especially during Covid-19.

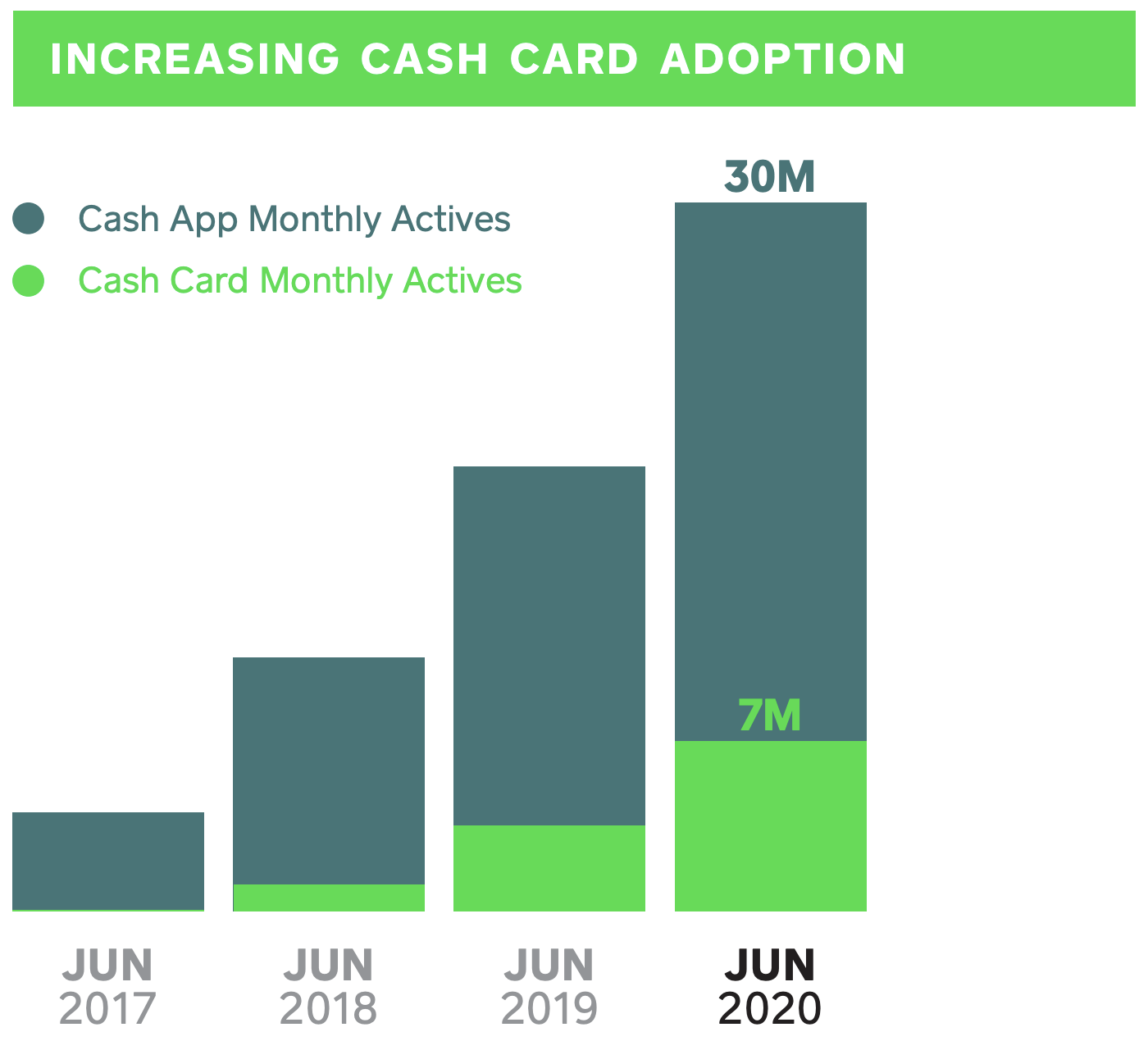

Square reported last week that Cash App had 30 million active customers in June, and even more in July. That June number appears to be up by more than 11 million customers from the same time in 2019, suggesting roughly 60% year-over-year growth, based on my analysis of this sparingly labeled chart included in Square’s quarterly shareholder letter (pdf).

Chart of the Day

Cash App started in 2013 as Square Cash, a simple peer-to-peer mobile payments service similar to Venmo. It never seemed to get a lot of attention in the tech industry, and doesn’t make much mention of the fact that it’s owned by Square, which was founded in 2009 by then-former (and now current) Twitter CEO Jack Dorsey.

But Cash App has evolved, adding a suite of useful and novel features over the years, and developing an irreverent yet relevant brand. As the pandemic has thrown the economy into a recession and accelerated the shift to digital money and e-commerce, Cash App is now likely one of the fastest growing banking services in the US.

The New Consumer Executive Briefing is exclusive to members — join now to unlock this 1,300-word post and the entire archive. Subscribers should sign in here to continue reading.

Hi, I’m Dan Frommer and this is The New Consumer, a publication about how and why people spend their time and money.

I’m a longtime tech and business journalist, and I’m excited to focus my attention on how technology continues to profoundly change how things are created, experienced, bought, and sold. The New Consumer is supported entirely by your membership — join now to receive my reporting, analysis, and commentary directly in your inbox, via my twice-weekly, member-exclusive newsletter. Thanks in advance.